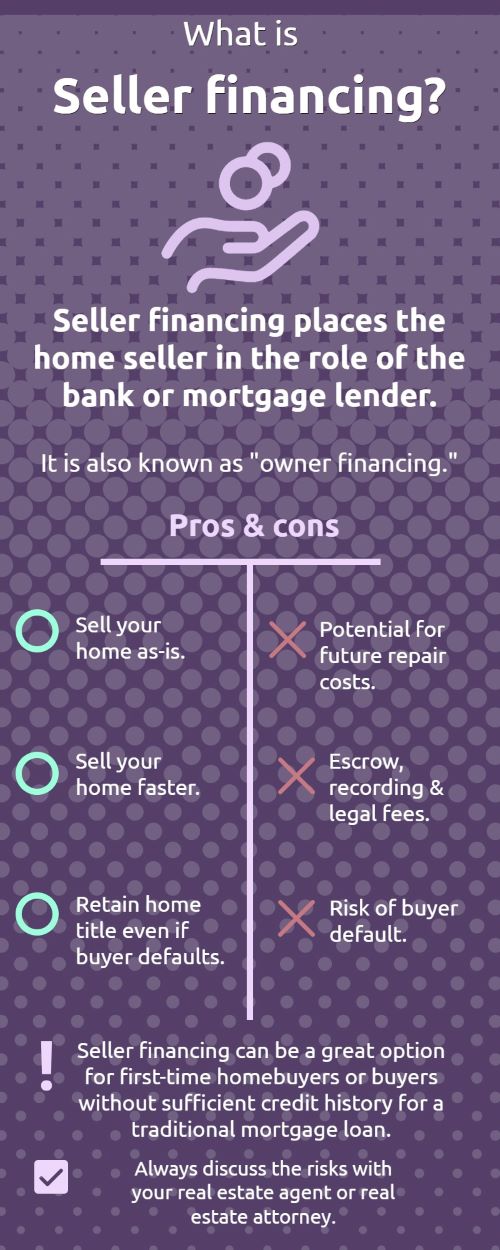

Seller financing is an option for buyers and sellers to work together without a traditional mortgage. Also called owner financing, this type of financing involves the seller providing funding for the home in the form of credit.

Since sellers are often more flexible with financial requirements than banks, this can be an excellent option for a buyer with subpar credit or other financial issues.

Here is some more important information about seller financing arrangements:

How does seller financing work?

In seller financing, the seller acts as the mortgage lender rather than a bank or financial institution. There are typically fewer closing costs involved and different requirements for home appraisals.

Types of seller financing agreements

Different types of agreements are available to fit a wide range of scenarios. The most common types are:

- Land contract.

- Assumable mortgage.

- Lease purchase agreement.

- Land loan.

- Holding a mortgage loan.

Mechanics of seller financing

In a seller financing agreement, both buyer and seller sign a promissory note with the specific terms of the loan. The buyer pays the amount back with an agreed upon amortization schedule, usually with interest. A seller financing deal often offers the short-term option of requiring a balloon payment within the first several years.

Tips to reduce the seller's risk

Just like a bank or mortgage lender, you take a risk when offering a seller financing agreement. If the buyer defaults on payment, you could be subject to serious legal fees. However, there are some steps you can take to serious legal fees. However, there are some steps you can take to reduce your risk as the lender and seller:

- Require at least a 10% down payment.

- Use a complete loan application just like a traditional lender would require.

- Work with a real estate attorney & knowledgeable real estate agent for help during the process.

Is seller financing a good way to sell your home? If you've paid off your existing mortgage, it can be a great way to make a sale in a tough market. However, many sellers would rather not take the risks. Ultimately, you'll have to weigh the pros and cons in your specific situation.

About the Author

Bob Hummer

Bob Hummer brings a wealth of experience with him; a practitioner in real estate in Northern Virginia since 1978, a Life Member of both the Million Dollar Sales Club and the Top Producers Club with over 2,500 Satisfied Families and President, Prince William Association of REALTORS in 1991. His experiences range from helping buyers and sellers attain their goals; to renovating historic homes on Capitol Hill; to counseling and assisting homeowners facing the loss of their home due to foreclosure. Since 1996, he has presented his free monthly Home Buyer and Home Seller seminars at the Woodbridge campus of Strayer University. In June 2023 he completed the Certified Probate Real Estate Specialist course and was awarded the designation CPRES. His goal is to assist individuals who inherited real estate and wish to sell. A former "Military Brat" and a retired Air Force Hospital Administrator, Bob has made more than 26 moves during his life and is extremely familiar with all aspects of a family relocating - whether it is across the street or across the nation.